FX settlement risk is on the increase, stemming from long-running issues in the industry coupled with new factors, including the ongoing Covid-19 crisis. We spoke to Arjun Jayaram, CEO and Founder of Baton Systems, about the role of fintechs and emerging technologies in helping address settlement risk in the trading lifecycle.

The Bank for International Settlement (BIS) has warned the markets that FX settlement risk is on the rise again. What do you believe is driving this increase?

There are a number of factors behind this rise. Firstly, the number of trades has increased dramatically in FX over the past couple of years. We’re now seeing much tighter bid/ask spreads, which means that sales and trading yields for banks have fallen. For banks, the only way to recoup that revenue is by increasing trading volumes. So there are more FX trades being conducted, but more trading means more settlement risk.

The second trend is the recent growth in trading exotic or emerging markets currencies. With the majority of emerging market or frontier currencies, CLSSettlement is not an option. This is a true risk that has increased tremendously because there is no alternative, there has been no viable settlement venue for doing a payment versus payment (PvP) settlement of these emerging currencies.

Volumes in some of the ineligible CLS currencies have grown markedly in recent years. Specifically, CNH, TRY and RUB are all very actively traded. What’s also interesting to note is that the major participants in these currencies include banks that are not always thought of as tier 1, global institutions.

Regulators require banks to hold additional capital to protect against this increased risk of unsettled trades. In turn, this puts downward pressure on the Return on Capital metric, which is so closely watched by the banks and their shareholders.

Why do you believe an alternative approach may be the answer?

If we look at the lifecycle of a trade, risk is being introduced into the ecosystem from the point a trade is made and it evolves from that point. As the BIS report highlights, many of these trades are settled in a non-PvP manner, but that is actually just looking at the final leg of the risk.

So while PvP is an important part of the counterparty settlement risk, there’s actually risk being built up from the point the trade is made all the way to settlement. We believe that the settlement risk creates an interesting challenge because different systems do not talk to each other and so there is a lack of visibility into the trade lifecycle between two banks. That is why at Baton Systems we always look at the entire lifecycle of the trade.

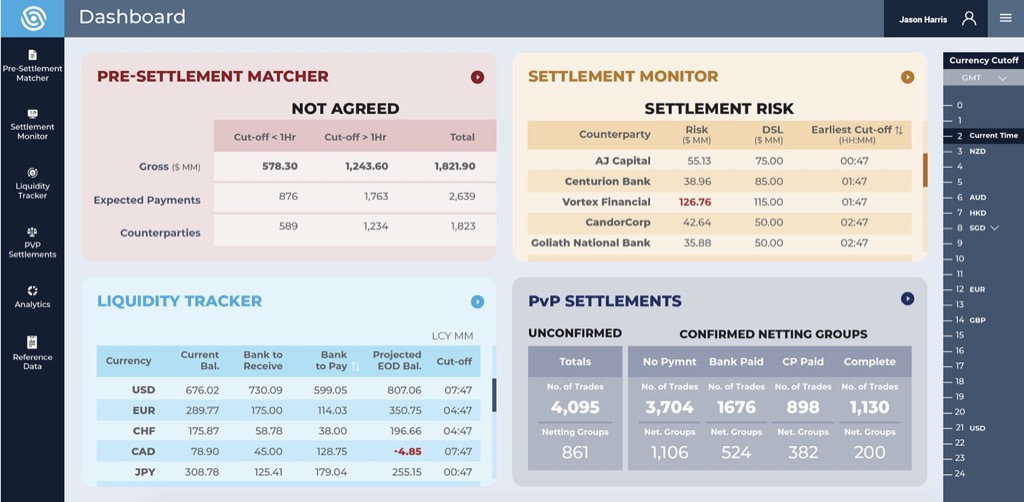

The Baton platform offers a management dashboard and automated alerts which provide real-time updates on key business functions and priorities

How can emerging technologies, such as Distributed Ledger or Machine Learning, be harnessed to improve the situation in reducing FX settlement risk?

This boils down to providing both visibility and control. These two elements are crucial to resolve settlement risk and some of the associated challenges around liquidity.

With newer technologies such as Distributed Ledger, we are able to see the full lifecycle of the trade. So we now know if and when a trade is going to be netted and at what point in time in the future it’s actually going to be settled. We can also check if the client has enough funds for the settlement so they don’t run into liquidity issues. Then finally, we also enable settlement in a PvP manner.

Essentially, we create three pillars to support the process. One is to help manage that risk during the entire lifecycle of the trade by providing a distributed ledger where all parties are able to see the same system of record, populated with the same data. The second pillar is our ability to provide clients with visibility of their funding sources and obligations, to better manage liquidity. Then the third part is enabling PvP between the counterparties when it comes to the settlement, which eliminates risk between them.

What has been holding back FX institutions from considering more widespread adoption of newer technologies or working closer with fintechs to find an alternative solution?

These trades are done in different trading venues which don’t tend to talk to each other, so one of the first things we have to do is source these trades from those venues. Yet even when we have that data, it doesn’t mean that the internal systems from the two counterparties that did the trade necessarily agree.

So it’s common to see heterogeneous data sources on the trade venues and heterogeneous sources within the systems of a bank. The next problem is that the collaboration tools being used by banks can be very old. Even today, we are still seeing settlements being managed by phone, email and sometimes, believe it or not, even by fax. It’s rare but we still occasionally see a system which is just a fax sent by one bank to the other to say what they owe. More common is trying to conduct this by email which is still extremely prevalent. In terms of operational management, this obviously creates a huge problem, particularly in cases where they are not in agreement.

The last issue is the settlement itself, particularly if one party has to pay before they receive and there’s a pre-funding requirement. This is where technologies such as a Distributed Ledger would be very helpful, and one of Baton’s capabilities is to integrate this technology with the trading venues and the bank ledgers. We don’t require them to make changes in their existing systems to benefit from our DLT. So it is a seamless solution to a problem that exists today.

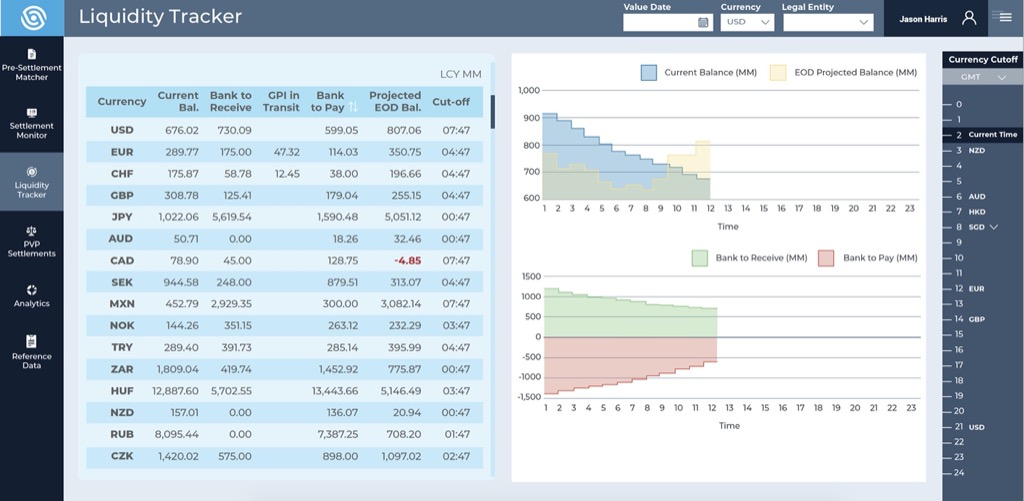

Liquidity Tracker: Maintaining available account balances and combining these with completed and pending incoming and outgoing payments

Are there any constraints on the number of currencies that you’re able to offer on the platform?

None. We use commercial bank money and not central bank money for the settlement process, so it is far easier for us to add new currencies on the platform when required. We built the platform to be truly currency and even asset-class agnostic – we also support securities in addition to currencies.

Currency coverage is one of the key constraints on existing PvP processes. CLSSettlement is a very efficient system and it has reduced a considerable amount of risk in the system. So it is a fantastic venue for settling between its 70+ members but it only settles 18 currencies. If you are not a settlement member or want to settle transactions where either leg falls outside of those 18 currencies, then you’re out of luck. CLSSettlement is also a batch-based system, so it only settles once a day currently. In contrast, Baton is now able to provide on demand settlements 24 hours a day. Instead of settling just once a day, you can settle every hour using our platform on any currency pair.

Could the industry be working more collaboratively together and with regulators, central banks or with fintechs to address this issue?

Yes, absolutely. There are some practical steps which the central banks can take to help. One thing that could really help is for these institutions to be more open by extending the settlement window to nearly 24 hours a day – and there would be huge demand for that. Membership criteria is also a huge issue. This is very restrictive, with many of the most important financial institutions not eligible to use certain central banks as a venue for settlement. For example, not even LCH can open an account with the US Federal Reserve because it is not domiciled in the United States.

Having said this, the central banks are certainly thinking creatively, with the Bank of England and the Federal Reserve having been notably active. In fact, the Bank of England is going one step further by having allowed fintech companies, such as Baton, to have access to central banks and facilitate settlement between two members.

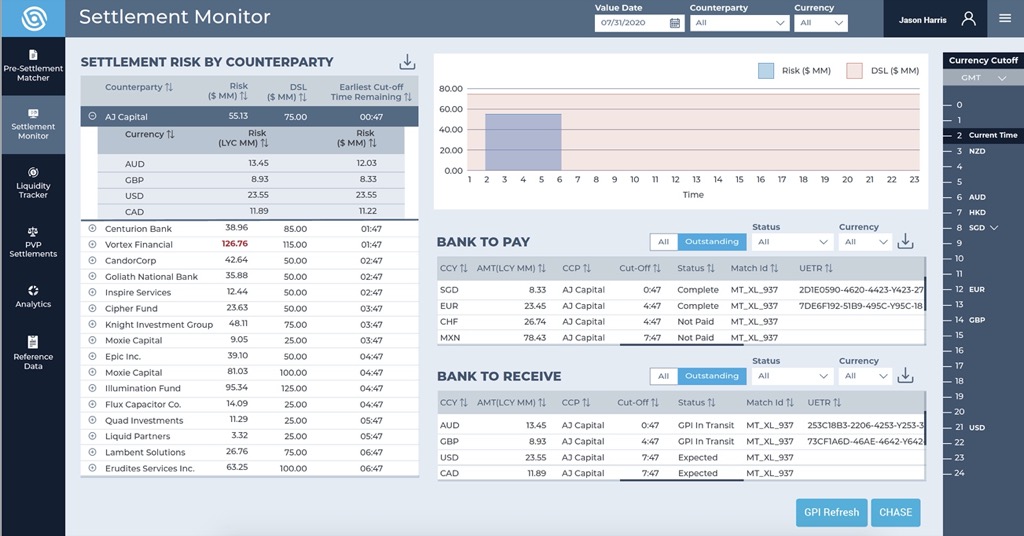

Settlement Monitor: Tracking and reconciling inbound payments, allowing intraday updates on settlement risk, and actual or potential failed settlements

Looking ahead, what impact do you think the Covid-19 pandemic will have on settlement risk in the FX markets?

It’s a constantly evolving crisis, but we do see a few trends emerging. March and April saw volumes shoot up significantly in FX. At the same time, we expected the stimulus measures taken by the central banks to further increase FX liquidity. Instead, what there was actually a shortage of liquidity due to a huge demand for US dollars.

The other interesting thing for the banks is the reduction in interest rates, which have dropped effectively to zero. That has had a profound impact on banks’ ability to generate net interest income, so they increasingly need to look at new venues or new markets to make money. The focus on these new markets will, generally, result in the more active movement of assets. This in turn has the potential to create more settlement risk between members. This is one of the most important macro trends that we see developing in the industry.

Following the initial volatility in March and April, we saw significant demand for our product. We believe this was a response to the crisis having brought into sharp focus for many in the market the full extent of these liquidity problems, settlement risk and operational inefficiencies. This is where the banks are now spending a lot more of their time and resources.

We also see an increasing shift to cloud-based technologies. This software is always up to date and it’s collaborative, allowing a fast and cost-effective way for the banks to improve their settlement risk efficiently. We see this as an almost inevitable and irreversible trend across the industry.