Corporate treasury is now facing change of a different magnitude. A fundamental shift in how it needs to operate, going beyond the heroic crisis response in recent months to building sustainable resilience into its operating model. The overarching objective is to prepare for a new way of managing risk across the evolving business landscape, supporting realignment in both distribution and supply chains.

Treasury now has a critical role to play in how it manages the usual risks associated with treasury and determines the appropriate actions needed to support business recovery. In our view, the current crisis for many businesses brought about by the pandemic response of governments and health officials across the world has become the unexpected tipping point for the full automation of treasury risk management processes.

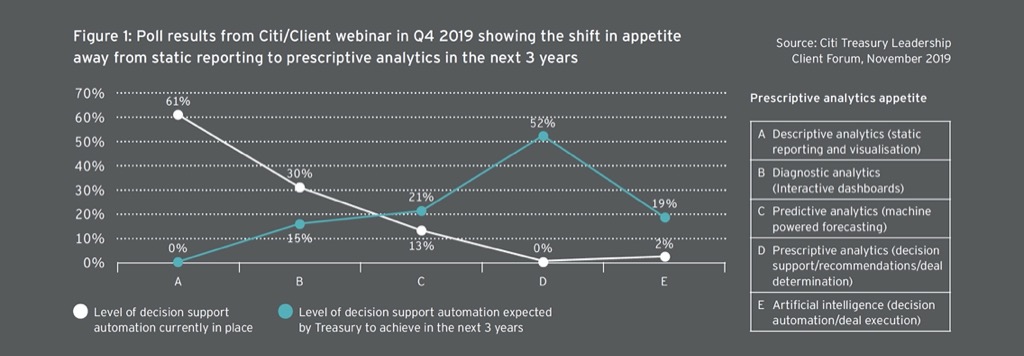

The appetite for prescriptive analytics — the provision of digitally enabled recommendations — has shifted further as a likely consequence of the challenge faced by treasury this past quarter. Before the COVID-19 outbreak, we were already seeing a measurable shift in client appetite for prescriptive analytics to support human decision making in treasury. With the onset of the current crisis, the automation of treasury is now for many a “must do” initiative to build the required resilience into their operation to manage risk.

Use of algorithmic techniques to predict and determine next action is increasing, and with this, we expect new value to be unleashed, offering treasuries the ability to digitalize at a pace and at a confidence level previously unachievable, but now necessary, to increase post-crisis resilience. The advent of new technologies and the evolution of financial services had already prompted treasury to rethink its future, but there is now a renewed focus by treasury to accelerate the delivery of its digital strategy to better support corporate objectives. A client webinar poll hosted by Citi in April 2020 indicates that over the half clients that joined are accelerating their digital strategy as priority. A further indepth survey was conducted in 2021 indicating a heathy appetite for algo risk management

Fully automating the fundamentals, coupled with prescriptive analytics to augment human decisions, is a well-documented requirement to realize the Future Smart Treasury. The mobilization of digitization initiatives is now prolific across treasury as a post-crisis response to building future operational resilience.

At Citi, we are running a number of initiatives in which we are collaborating with our clients and their technology partners with the shared objective to empower treasury decision-making by digitalizing processes using algorithmic techniques. There is opportunity now to reimagine treasury through this symbiotic relationship between people and data-fuelled predictive and prescriptive algorithms, with some even moving to consider that final step in the journey to smart treasury: deploying AI-enabled machines to execute next actions on their behalf. Establishing trust in machine–led execution of next action for risk mitigation is expected to come about through collaborative experimentation across corporates, banks and technology partners.

Smart treasury processes

The flow diagram in Fig 3 breaks out the logical steps involved in the build-up of smart treasury processes. Firstly, treasury policy is validated and combined with forecasted currency position (and variance) fed into a prescriptive analytics engine to determine appropriate hedging action. Secondly, recommended actions are inferred, providing decision support to treasury risk managers. Thirdly, what follows is extending to offer auto-execution of the prescribed actions, with feedback loops to support machine learning through subsequent iteration. The result delivers AI-enabled currency risk management. Policy validation moving from an infrequent manual response to a more frequent continuous digitized process offers resilience to allow for market disturbances and consequential currency exchange volatilities.

Transitioning to a model of continuous validation of policy sufficiency

Let us start by defining what we mean by continuous validation of policy sufficiency:

- The availability of a toolkit to deliver against policy objectives.

- Sufficient visibility, connectivity and machinery for continuous monitoring of the suitability of deployed instruments.

Together, these ensure policy flexibility sufficient to meet the prescribed risk mitigation action.Before we describe how such continuous validation can be brought about, let us briefly remind ourselves how treasury can create a risk management policy today and what characterizes best practice. A successful program relies on identifying and quantifying risk, consistent with a risk-based approach.

Treasury and the business are closely aligned in setting hedge objectives and setting risk tolerances. They design an optimal hedge solution to reduce corporate-wide earnings-at-risk to acceptable levels. And they have established a high level of resources and technological infrastructure around risk management often under a centralized treasury concept. Applying these basic components, the process for a best practice to managing financial risks becomes the following five steps:

- Determine overall business objectives. Business objectives and factors that might influence risk management objectives include: expectations of or promises made to equity analysts in regards to financial performance, marketing and product pricing strategies, competitive position in an industry, industry trends, and business philosophy and risk preferences

- Identify and measure risk. This involves identifying exposures based on a functional currency approach, categorizing exposures (i.e. accounting, economic), designing methodologies for quantifying the potential impact of market prices on an entity’s financial performance, and performing analysis to determine the overall risk to the company.

- Set risk tolerances and hedge objectives. Based on the overall business objectives of the company, define how much risk the entity is willing to tolerate and the overall objectives of the hedging program. Clearly articulate these objectives in a formally approved risk management policy. Define the procedures necessary to support the risk management process.

- Design a strategy and implement. Evaluate different hedging alternatives in terms of instrument selection and management style. The choice of strategy should be consistent with policy objectives and subject to constraints (i.e. accounting, lack of resources, and dependability of forecasts).

- Track, measure and report performance. Determine whether risks have been reduced below approved risk tolerances. Assess the effectiveness of hedging relationships periodically as required by your applicable accounting standard. Benchmark performance against an actionable, passive, and sanctioned hedging alternative. Report hedging results to senior management.

These steps define the manual process today for managing risk and applying appropriate hedging solutions based on company policy and objectives. This is a risk-based approach because many of the best practices rely on the quantification of risk as the basis for designing an appropriate response. However, it is impossible to respond in a timely manner to a potential risk if you are unable to measure, visualize, and quantify your risk profile on a continuous basis. This is where technology comes into play. The future of risk management best practice relies on the ability to continually, or regularly, monitor and validate the appropriate instrument selection and adjusting the risk mitigation accordingly.

Table 4 captures some of the benefits of moving to a continuous risk management process. As part of this initiative at Citi, we expect that best-in-class treasury will transition to a continuous digital monitoring of policy to provide sufficient flexibility and built-in resilience to market disruption.

Determining actions needed by treasury to deliver risk management objectives

The appropriate set of actions and instruments needed to mitigate currency exposure to risk-policy levels and ratios is determined by combining the forecast of currency exposure over time with those policy objectives. The effectiveness of the hedge put in place directly correlates with the accuracy of the forecasted exposure. Inaccurate forecasted exposures can lead to the frequent adjustment of placed hedges. Such adjustment actions can depend on corporate cash reserves and whether the adjustments themselves generate a positive or negative cashflow.

We have already discussed the opportunity to continuously monitor risk policy sufficiency through process automation. We now examine the increasing adoption of algorithmic forecasting and the auto-determination of required next action, where determining required next action incorporates forecasted currency position and forecasted variance within risk policy parameters into a prescriptive algorithm.

The case for algorithmic forecasting

Many corporates today face challenges in preparing accurate forecasts. Fractured data sets and technology infrastructure deficiencies are driving manually intensive processes. In a recent benchmark study at Citi of over 400 treasury professionals, approximately half report that their treasury management systems do not fully support financial risk management processes, with 63% noting that their TMS is not fully integrated with their ERP, and 77% lacking full integration of their ERP with banks.

Traditionally, and primarily for these reasons, forecasting has been a mostly manual process with people gathering, compiling, and manipulating data within spreadsheets. With more and more data available, this manual forecasting approach has become an unwieldy, time-consuming process that makes discerning what is important next to impossible. As a result, individuals tasked to execute this process often resort to their own intuition and judgement, which opens the door to unconscious biases and conscious sandbagging.

Corporates are shifting away from traditional techniques to forecasting processes that involve people working symbiotically with data-led predictive algorithms replacing the manually intensive spreadsheet-based aggregation of predictions from business units. Algorithmic forecasting solutions are becoming increasingly available in the market from technology companies, such as Citi Ventures-invested Cashforce, and those solutions tend to have the following attributes:

- Statistical models best fit to past commercial activity that describe what is likely to happen in the future, and data science deducing models to predict based on historical flows and market data.

- Machine learning algorithms incorporated to course correct and improve forecast accuracy over time, learning from previous cycles.

- Combining with human intelligence to evaluate machine conclusions providing another feedback loop to further enhance the algorithms.

Auto-determination of next action

Forecasted currency risk position with a variance measure by currency over time arising from the algorithmic techniques described above provides one set of inputs. The second set of inputs is a measure of currency risk profile/appetite for the treasury: namely, risk management instruments allowed and stated treasury objectives such as cost optimization, VaR tolerance, and/or best rate achieved.

With these two sets of inputs, logic creates a prescriptive algorithm to deduce the necessary hedging actions. The output of such algorithms goes beyond simply offering an opinion and extends to providing an evidence-based set of outputs, providing the rationale as to the why the recommendations were made, offering full transparency for human/machine trust creation.

Historical back-tested data and instrument profiles are used to suggest optimal trade recommendations. An important component of this prescriptive algorithm is its ability to incorporate forecasted error, which, fed into the algorithm at the same cadence as the algorithmic forecasted currency positions, produces an optimum outcome. This, we expect for some, may approach a near-real-time feedback loop of forecast error, enabling a high-frequency validation of the hedging policy and resulting in a possibility for a near-continuous tracking of hedge effectiveness through market disturbance events.

Currency movement forecasting models that provide the necessary signals to risk managers to adjust their hedging programs form part of an extensive suite of emerging decision-support tools. The availability of tools that forecast the direction of specific currencies within a specific time horizon has increased, providing needed supports for individuals making more refined hedge decisions.

With the combination of algorithmic forecasting (as more specialized vendors enter the market), advanced currency movement forecasting models, and algorithms to determine the best next action, coupled with the automation of policy validation practices, the advancement of decision-support tools for risk managers to determine and prescribe next action is accelerating. The next step for corporate treasury is to identify the most cost-efficient means of realizing currency risk management objectives through the auto execution of prescribed next actions.

Realize the recommended actions via intelligent automation of trade execution

Perhaps the most common form of automation in currency risk management is the integration of a company’s TMS with an electronic FX execution venue. Most companies tend to be satisfied executing through FX liquidity aggregators (e.g. FXALL, 360T), citing key reasons such as consolidated reporting, competitive pricing, and the ability to efficiently distribute their FX wallet among their banking partners.

Direct connectivity with banks tends to happen only when there are gaps with these aggregators. Typically, that’s due to unavailability in specific markets (such as highly regulated countries), specific instruments (such as complex options), or channels (such as algorithmic execution). Therefore, only the most global of banks have direct connectivity with clients, who tend to be the most global of corporate treasuries.

The process steps covered by this intelligent automation are:

- Required FX hedges generated in the TMS.

- Transmit FX hedges to the desired execution venue, typically via an API.

- Log on to the user interface of the execution venue.

- Review pricing provided, select the respective liquidity provider and transact.

- Transmit completed FX hedges including both confirmed price and FX counterparty details.

Typically, as well, the exposures in step 1 are tagged in such a way that the associated hedges in step 5 are identifiable from a hedge-accounting point of view. An increasing number of companies are skipping step 4 either because they view that best execution is achieved by the multiple liquidity providers bidding for the deal, or because they view that associated costs have been pre-agreed with their respective liquidity providers, in the case of a direct connectivity.

As discussed, though, the process that leads up to step 1 is still predominantly manual and cumbersome for a treasury. As risk management gets more prescribed via the real-time algorithms described in this article, hedge determination is made fully automatic. Connecting the results of prescriptive analytics to initiate automated hedges will be the new normal. As forecasts are adjusted on a real-time basis, hedge adjustments will naturally be more frequent but smaller in size.

Importantly, treasuries will also look to step away from typical hedge cycles (usually monthly) to one that is happening constantly. The shift of focus for a corporate treasury at this phase will be less on price discovery and more on ensuring that in this new touchless environment, there are ample failsafe mechanisms to ensure that the right people are notified at the right time for any manual intervention.

To elaborate further, things can go wrong during auto execution for a multitude of reasons such as lack of credit allotment by the price provider causing rejects, latency in the network causing a lack of response and code errors that result in the duplication or incorrect notional of trades being sent. Prescriptive analytics may provide the most accurate of recommended actions, but poor management in the execution phase can lead to significant losses when issues are not addressed in a timely fashion.

Other considerations would also need to be made, such as the impact of liquidity when a company transacts, as attempting to transact large transactions at the wrong time can be costly — particularly with too many liquidity providers.

Another example is avoiding concentration risk by ensuring that counterparty exposures are managed evenly between banking partners. Therefore, the algorithms required to be deployed in this phase will need to incorporate these crucial parameters and not just focus on achieving best price. That said, auto execution is a fairly mature field and already firms have begun the process of shifting parts of their portfolios into a rules-based environment.

With the right structured test plan to iron out all foreseeable issues and robust failsafe mechanisms in place, a typical treasury should be able to find sufficient comfort to kick things off. It is therefore not too far away. With the advancements of prescriptive analytics discussed in this article, this final linkage to execution paves the way for the era of Artificial Intelligence in treasury currency risk management with full end-to-end intelligent automation.

Towards a smart treasury future

The innovations described in this article are some of the key components of the suite of initiatives at Citi targeted to support our clients’ smart treasury aspirations. Future treasury will be defined not only by the automation of repetitive tasks but also by the utilization of prescriptive analytics to determine best next action. Treasury that is sensitive to market fluctuations will be able to offer a more resilient function that is more capable of dynamically adjusting to future shock events.