By Sam Romilly, FX Global Market Management, SWIFT

The growing amount of FX settlement risk is of concern to all in the financial industry and the nature of the challenge in its size, and complexity, is significant. The industry settles over $18 trillion each day1 resulting from a variety of FX instruments, each with their own settlement periods, with over 1,000 currency pair combinations, traded by 1,000s of financial firms across over 100 different platforms, spread over 200 jurisdictions across different time-zones. This makes clear the need for up to date, and accurate, data on the FX post trade process. The good news is that information on a significant percentage of the daily $6.6 trillion2 of value traded can be derived from the FX confirmations sent over SWIFT. Over 6,000 financial firms send FX confirmations between themselves, and to the 2,000 corporates and investment managers indirectly connected to SWIFT via the FX post trade platforms. Data extracted from the million FX confirmations sent each day is now available as a dataset to complement data already available from CLS.

The following description of the confirmation process illustrates how this dataset can be an invaluable tool to better understand FX settlement risk. The FX Global Code advises that trades need to be confirmed whether settled gross, or netted. Each party should also match the confirmation sent to the one received. If there is a mis-match then one of the parties will cancel their original incorrect confirmation, and send a replacement confirmation. This process continues until both parties have correct matches. If the matched confirmations are to be netted, then there should be a procedure to confirm the bilateral net amounts in each currency, at a predetermined cut-off point. The SWIFT FX dataset adjusts accordingly for the cancellations, and so effectively contains details of all matched confirmations. As such, an accurate simulation of calculations for netting, and counterparty settlement exposure, is now possible. Hypothetically, this dataset, if it were to operate in real time, could be the basis of a solution to monitor counterparty exposure values, and even calculate bilateral netting amounts at the relevant cut-off times.

This dataset is only available to SWIFT users for their own data, and the market level data provided is under strict controls to guarantee confidentiality and anonymity. It contains details of confirmations on a trade and value date basis, and can be provided on a daily basis. Data extracted from these confirmations is unique, consistent and unbiased. The granularity of the SWIFT FX dataset enables analysis at the level of currency pair, instrument type, region, business segment of the trading parties, and by value, and number of transactions, each day. A SWIFT user with access to this data can easily find out their daily counterparty exposure across all their branches, and across all the branches of their counterparty. They can also see potential reduction in risk if the counterparty were to become a CLS third party, and can use it to help select the counterparties, and currency pairs, they wish to bi-laterally net.

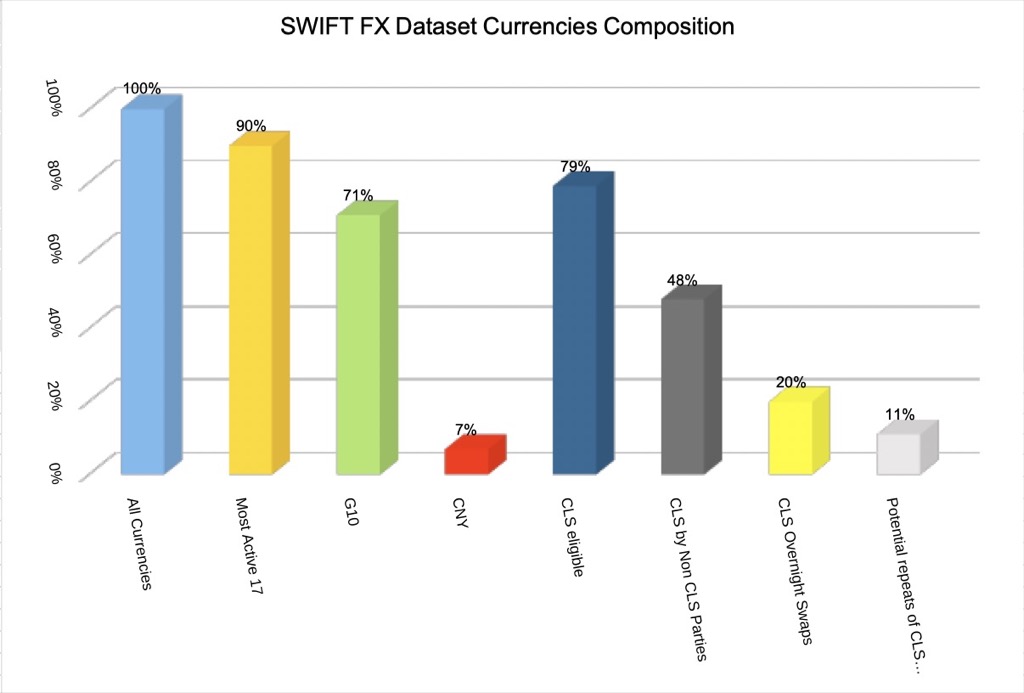

Figure 1

The Figure 1 chart gives some high level views of the FX currencies confirmed over SWIFT. We estimate that around 90% of the FX confirmations sent over SWIFT settle outside of CLSSettlement, as trades that settle in CLSSettlement are usually not confirmed over SWIFT. It may be a surprise then to see that 79% of the confirmations sent over SWIFT are to confirm trades for CLS currency pairs. However, there are several quite valid reasons why such trades do not settle in CLSSettlement. For instance, one of the parties to the trade may not be a CLS member, or a CLS third party. Another reason is that the FX instrument could be a Non-Delivery Forward or an Option. Finally, if the FX trade is a give-up between a hedge fund and prime broker, or if it requires a same day settlement, then it is unlikely to be instructed to CLSSettlement.

NETTING DATA RESULTS

Where the data becomes even more interesting and revealing is in the insights it can bring around bi-lateral netting. The use of netting to reduce settlement risk is an acknowledged best practise, and CLS have a centralised netting service – CLSNet – open to any financial firm via their preferred SWIFT connectivity channel. BIS estimate that use of bi-lateral netting today already achieves up to 20% reduction of settlement risk1.

The following overview illustrates how the SWIFT FX dataset can help any bank to have a better understanding of the underlying components of their FX settlement risk, and to quantify the benefits possible from increasing their use of netting, and of CLSSettlement.

We first created a settlement risk dataset based on (i) FX confirmations sent for all currency pairs during a 24 hour period in August 2020, (ii) for the instrument types spot and swap (the opening leg only), and (iii) excluding confirmations sent between branches of the same firm.

For illustration purposes we calculated3 the total gross of the Buys and Sells per currency pair to give the gross settlement value of all the confirmations in this dataset. It is possible to now derive the actual maximum amount of FX settlement exposure per counterparty of a typical top tier bank. It is also possible to calculate the amount of settlement risk removed if a trading counterparty were to become a CLS third party. We calculated the total net across all branches, currencies and counterparties, which showed it was possible to achieve a 60% reduction in the gross settlement amount. In terms of the BIS report totals this means that a theoretical reduction from $10 trillion to $4 trillion settlement risk could be achieved with bi-lateral netting. Obviously, this is just a theoretical maximum but, when looking at the data across top tier banks at a branch level, we still see impressive gains possible from netting. However, the dataset also shows that a branch of a top tier bank can have as many as 500 counterparties, dealing in over 300 currency pairs. The number of combinations this entails would appear to make it impractical to net everything especially given that banks continue to rely on e-mail to agree the net amount.

We therefore calculated, for a typical top tier bank, the ideal number of currency pairs, and netting counterparties, and made the following findings. First, if such a bank were to net the top 20 currency pairs, across all counterparties, then they could achieve a reduction of settlement risk of 53%, and 15,000 payments reduce to around 3,000. Second, if they were to net with the top 20 counterparties, across all currency pairs, then there is a reduction of settlement risk of 60%, and 13,000 payments reduce to just 900.

Third, if they were to net the top 20 currency pairs, with the top 20 counterparties then this would cover 70% of all trades, reduce settlement risk by 50%, and 12,000 payments reduce to only 350. So, it is clear that netting not only has the potential to reduce settlement risk significantly, but can bring many operational and cost benefits due to the substantial reduction in the number of payments.

The above type of analysis shows how SWIFT data can help make the case for further investments to reduce FX settlement risk. The SWIFT FX dataset is available to any SWIFT user, and we are ready to undertake customised investigations via our professional services teams.

- BIS Quarterly Review, December 2019 https://www.bis.org/publ/qtrpdf/r_qt1912.htm

- BIS Triennial Bank survey https://www.bis.org/statistics/rpfx19.htm

- All calculations and estimates in this article are research in progress by the author that are published to elicit comments and to encourage debate.