By Richard Willsher

SWIFT’s Global Payments Innovation (gpi) messaging has become the norm for cross-border interbank payments but the innovation continues.

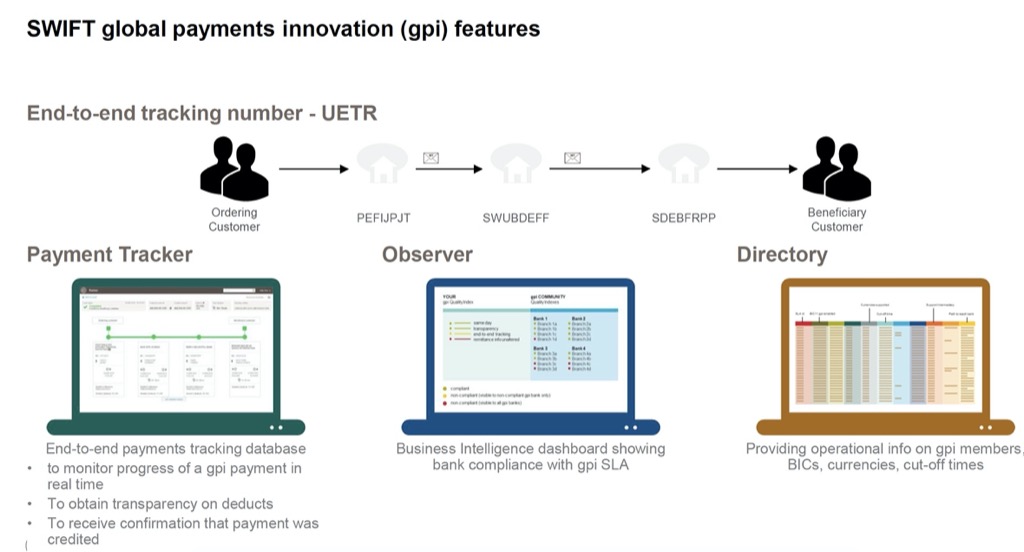

Launched in 2017 to offer a fast, transparent and secure cross-border payment platform, gpi provides customers with traceability of their payments. The service enables predictable settlement times, transparent bank fees and FX rates. The key building block of the system is SWIFT’s MT103 message whose “tags” define the details of payment and the counterparties involved.

Highly successful as it has proved to be over millions of payments, SWIFT in 2018 added an

important new ingredient, the UETR (Unique End-to-end Transaction Reference)

UETR and the MT 202

Highly successful as it has proved to be over millions of payments, SWIFT in 2018 added an important new ingredient, the UETR (Unique End-to-end Transaction Reference). This is effectively a stamp attached to each individual payment that enabled it to be tracked to wherever it was in the payment process. Moreover, to add a further traceability and transparency, the UETR can be published to the cloud where, as SWIFT’s Strategic Relationships – Capital Markets leader Matt Cook explains, “A GUI or API can now interrogate where a payment is in real-time, the status of that payment, when it’s arrived at an institution, when it’s been released, or when it’s going to be credited into the beneficiary’s account. This is a quantum leap.”

Next came the addition of the MT 202. Matt Cook explains that a consultation carried out among its financial institution users surprised SWIFT as it became clear that MT 202 messages are used to substantiate a large proportion of intra day funding and in particular FX payments that are made bi-laterally outside of CLSSettlement.

Therefore, when SWIFT started to trial its new gFIT – gpi for Financial Institutions Transfers – offering, MT 202 was an essential component. “As of November this year,” says Cook, “entities on SWIFT will be able to say “Actually we’d like the MT 202 included as part of our gFIT service” and so for the first time they’ll be able to have the entire payment flow on gpi; completely trackable and transparent with service level agreements attached.

gFIT pilot

SWIFT is currently piloting gFIT among a small but significant group of major FX market participants. JP Morgan is one of these and we wanted to find out how it’s working for them and what the impacts of gFIT could be, especially for settlement risk. We spoke to Sarah Dunning, J. P. Morgan’s Commercialization and Communications Lead for Clearing Transformation, Wholesale Payments and her colleague Matthew Smith, Executive Director, CIB Operations.

“We’ve been delighted to be able to use this data to the benefit of our clients,” says Sarah Dunning. “We have a large wholesale payments franchise covering so many external financial institutions clients that will really benefit once MT 202 tracking comes into effect with gFIT. It’s been really exciting for us to be involved with this programme. It wasn’t very difficult to convince our internal departments that they would actually benefit from this as well, because seeing the reality of tracking MT 103s end-to-end, it’s definitely something that is of huge interest such as in FX or securities settlements. In any treasury management function, the ability to track a MT 202 from end-to-end, offers enormous potential.”

Matthew Smith agrees. “Having access to the real-time data of where our funds are, incoming and outgoing, will enable us to manage positions more effectively. If we take less liquid currencies for example, then it will enable clients to meet their obligations. Some of these currencies don’t have overdraft facilities where certain countries have regulatory restrictions that prevent them. So, if you do not have the money in your account, you cannot make these payments. Finding out where the payments are, giving that transparency, will enable positions to be managed more effectively.

Another useful thing is the data,” Smith continues. “That we can analyse historical data that we’ve got from gFIT, we can see where have payments been held up, why that has been the case, and how we can we resolve that for the future.

So, it’s about client education. We can ask them to format their message slightly differently so that it goes through straight-through processing rather than getting held up along the way. So, it’s quicker, cleaner, more effective, and therefore reduces friction, which is the goal overall.”

In summary, SWIFT is harnessing data within gFIT and MT 202 to control settlement risk, simply by providing certainty and transparency as to where payments are and what may be holding them up.