By Sam Romilly, FX Global Market Management, SWIFT

SWIFT commissioned this e-Forex magazine supplement because of the size of the outstanding risk, and the complexity of the problem. Our objective was to bring together some of the top practitioners, solution providers, and thought leaders to really dissect the problem, to examine what solutions exist today, and to see what could be done in the future. Addressing FX settlement risk will require major improvement, and evolution, of the current methods. It could also potentially require radical paradigm shifts to alternatives such as pre-funding, collateral and new technologies.

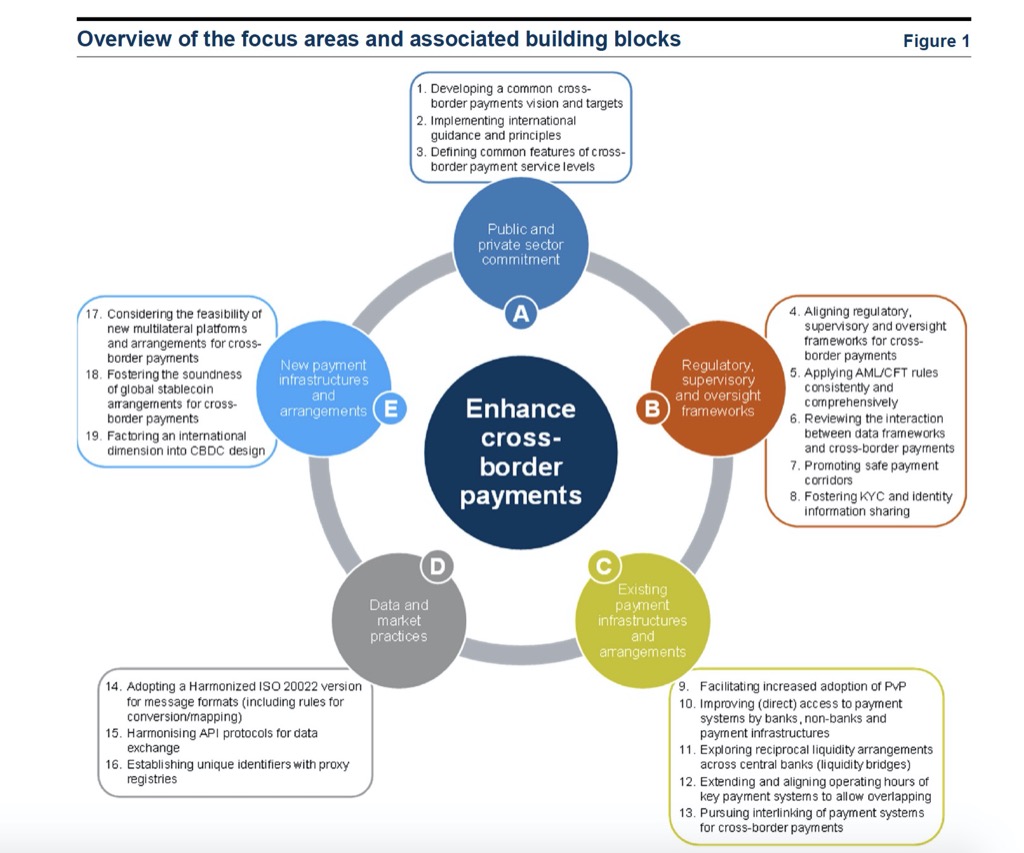

This has turned out to be good timing as the FSB has just released their Stage 3 report on enhancing cross-border payments where one of the ‘Building Blocks’ outlined is titled “Facilitating increased adoption of PvP” that directly addresses the topic of FX settlement risk. (See Figure 1 below) The FSB will present a consolidated report to the G20 each year to report on progress, and to review actions and timelines.

Currently CLS removes around $5.5 trillion of settlement risk each day, which leaves, according to BIS figures, at least twice this amount to settle each day by other means. BIS estimates that the proportion of trades with PvP protection appears to have fallen from 50% in 2013 to 40% in 2019.

Some underlying reasons for this are: (i) the long-term upward trend in overall volumes, (ii) the increasing share of prime brokerage, (iii) the increasing use of swaps, and (iv) the trading volumes of non-CLS currency pairs where the share of emerging market currencies rose to 23% in 2019 from 19% in 2016. The increasing use of the swap instrument may well be the more significant factor behind this increase in settlement risk given its take-up by the small regional banks, who are less likely to use CLSSettlement, and the fact that each swap trade implies four settlement legs.

A common theme across all the articles is the need for more industry data to understand how the 60% of those FX obligations without PvP protection actually settle. Whilst a significant proportion would be via the correspondent banking process, other settlement mechanisms exist such as cross account movements for the “on-us” settlement process, internal account movements for intra-group trades, and back-to-back movements for the prime broker ‘give-ups’ process.

CPMI: Enhancing cross-border payments: building blocks of a global roadmap – Stage 2 report to the G20 (July 2020)

Another theme is the need for inter-operability between new alternative settlement solutions being contemplated. On the one hand, central banks are exploring PvP settlement solutions based on new models such as the ‘synchronisation’ of RTGS cash movements, extended opening times, and use of wholesale crypto-currencies. On the other hand, FinTech companies are promoting new PvP solutions based around smart contracts, distributed ledger and use of escrow accounts.

However, in many cases such innovations introduce a dependency on pre-funding which has implications on liquidity as funds need to be available at trade date rather than at value date. Any ‘same day’, or even ‘instant’, settlement needs to address this issue of liquidity. CLS has a significant advantage as multilateral netting reduces pre-funding requirements by up to 96%. In addition, CLS offers a liquidity management In/Out swaps facility to reduce funding requirements by a further 3%.

This then is the quandary faced by some of these new models. How to align prefunding of FX transactions with the need for liquidity. There are many innovative ideas such as intra-day borrowing, posting of collateral etc also discussed elsewhere in this supplement.

These new models are more likely to be complementary to CLSSettlement than alternatives, but inter-operability will be key to their success. There also still remain significant opportunities for growth in CLS based settlements by increasing the number of third party clients, as can be seen and quantified, in the SWIFT FX dataset.

| The introduction of gpi for the MT 202 financial transfer instruction, the gFIT service does not take away settlement risk but it makes a major improvement to the monitoring and management of it |

|---|

The crucial step in FX settlement are the actual payment instructions, both for netted FX transactions, and for FX transactions that will settle gross. Whether settled gross or settled net, each party will send an outgoing payment, and will expect to receive an incoming payment. This is of course the heart of the FX settlement risk as if the outgoing payment is sent, but the incoming payment does not arrive, then a settlement failure occurs. And the amounts involved can be large as verified by our SWIFT FX dataset where we can see the average EUR:USD gross settlement exposure between any two players for every day in the year.

The introduction of gpi for the MT 202 financial transfer instruction, the gFIT service, means that FX parties can now monitor both the progress of the payment they sent for the currency they sold, as well as the incoming payment they expect for the currency bought. Whilst this does not take away settlement risk, it makes a major improvement to the monitoring and management of the risk, especially if it were to be combined with bi-lateral netting solutions. gpi is in the process of transforming the correspondent banking payment processes.

Looking forward to the future this basic principle of linking the two payment legs together via gpi could support new PvP based solutions. For example, if a crypto-currency were to become the settlement mechanism for a FX trade it would still require links to accounts to know when both parties have made their payments in order to transfer ownership. Similarly, a solution based on an escrow account arrangement would be able to release funds based upon receipt of gpi confirmation of credits for each payment leg. gpi users could themselves set-up a market infrastructure to offer PvP services based on the updates for each payment leg received from the gpi service. The importance of data and of visibility on assets is clear, and to this end SWIFT shall continue to extend the transaction management and data capabilities of our platform.

FX settlement risk is an industry critical subject and we hope that this e-Forex supplement has helped to contribute to the debate. Conversations and analysis will certainly continue and SWIFT looks forward to be part of the dialogue. We also look forward to your comments on this supplement.