Foreign exchange markets are among the largest and most liquid in the world, with daily turnover exceeding $7 trillion. Yet for businesses and institutions with operational FX needs – paying suppliers, repatriating earnings, funding payroll – conversion remains persistently expensive. Despite decades of electronification, algorithmic execution, and intense competition, these costs endure. This persistence is not necessarily a failure of competition. Rather, it reflects the structure within which FX markets currently operate.

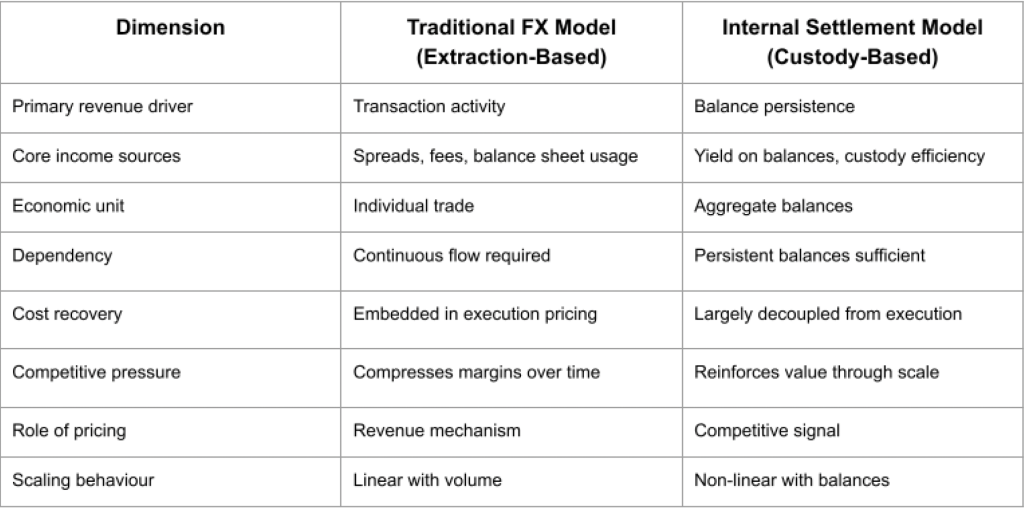

A defining feature of that structure is the separation of price discovery from settlement. When settlement sits outside the trading venue, every conversion requires value to move across balance sheets, jurisdictions, and correspondent systems, often with delayed finality. These processes introduce capital usage, credit exposure, and operational overhead that cannot be eliminated through execution alone. They must be recovered somewhere in the system. As a result, venues monetize conversion rather than price discovery. Competition can redistribute these costs, but does not fully remove them. As long as settlement remains external, FX pricing continues to reflect these underlying frictions. Persistent cost is therefore structural, not anomalous.

Yield as the catalytic force

Internal settlement removes many of the structural constraints that sustain FX pricing. On its own, however, it does not fully explain the direction or pace of change. A key enabling factor is the emergence of yield-bearing settlement balances. In traditional FX systems, balances required for settlement are often economically inefficient. Capital tied up in prefunding requirements, nostro accounts, and fragmented custody structures typically generates limited return. Participants are incentivized to minimize balances and accept the friction of repeated movement.

This dynamic shifts when settlement balances become economically productive. Where balances generate yield, holding funds within the system becomes more rational. Participants concentrate balances where yield and pricing efficiency are highest. Over time, custody persistence emerges as a natural consequence of these incentives. As balances persist, the system acquires an additional source of economic value. Execution no longer needs to fund infrastructure to the same extent. Under these conditions, internal settlement becomes progressively more attractive, as it allows the system to capture and retain the economic value associated with balances. This dynamic becomes self-reinforcing. In this way, what was once a cost centre – custody – can become a source of structural advantage, encouraging greater participation and liquidity provision.

Internal settlement and the repositioning of FX economics

Consider a system in which settlement is internal to the trading environment. Value transfer occurs within a shared custody and accounting context, achieving finality without correspondent chains, prefunding requirements, or bilateral credit extension. Under such conditions, the economics of FX shift. Settlement costs no longer need to be fully anticipated and embedded in pricing prior to execution. Execution becomes less dependent on balance sheet constraints. Price discovery can increasingly reflect competition on price quality rather than the ability to intermediate settlement risk or deploy capital. The resulting dynamic is mechanical. Tighter pricing attracts flow. Increased flow deepens liquidity, further tightening pricing. Competition becomes less constrained by the need to recover settlement costs through execution.

Pricing compresses toward marginal cost as the need to recover settlement friction diminishes. Where economic value accrues from balances held within the system—rather than from transactions themselves—execution pricing may, in some cases, extend beyond zero. Trading activity can improve price discovery, attract liquidity, and contribute to balance persistence, making it economically rational to incentivize, rather than charge for, certain forms of execution. This represents a shift in economic orientation. In traditional FX systems, trading activity is often the point at which costs are recovered. In internally settled environments, trading activity can instead support the accumulation and reinforcement of balance-driven value, allowing price discovery to operate more directly on competitive merit.

Custody as the dominant scaling variable

This shift has implications for how FX infrastructure scales. In conventional systems, economics are largely transaction-driven. Revenue depends on volume, and activity must be continuously stimulated. In an internally settled environment, the primary state variable may shift toward custody. Transaction volume is inherently variable. Balances, by contrast, tend to persist. As conversion friction declines, the incentive to move funds across venues diminishes. Balances can accumulate where pricing is consistently competitive and settlement is final. That accumulation becomes self-reinforcing, deepening liquidity and improving pricing. This may produce increasingly non-linear economics. The marginal cost of additional balances can be relatively low, while the economic value associated with those balances continues to grow. Under such conditions, the system depends less on transaction volume and more on balance persistence.

Why this transition may not be incremental

Incumbent FX infrastructure is built around external settlement. Revenue is derived from spreads, transaction fees, balance sheet usage, and the facilitation of value movement across institutions.

Incremental improvements – such as tighter spreads or faster execution – operate within this structure. They may reduce visible costs, but do not fundamentally remove them. Settlement remains external, and pricing continues to reflect associated frictions. Internal settlement alters where economic value resides. It reduces the need for trading activity to fund infrastructure. This is not an incremental improvement, but a shift in underlying economics.

Hybrid approaches may prove difficult to sustain. Systems that partially internalize settlement while retaining transaction-based revenue models may need to reintroduce costs elsewhere. Conversely, systems that reduce or eliminate fees without alternative economic support may face sustainability challenges. As a result, an intermediate state between these models is likely unsustainable.

Reallocation of economic value

The transition toward internal settlement does not eliminate economic value in FX infrastructure, but redistributes it. In traditional models, revenue is derived primarily from transaction activity – spreads, fees, and balance sheet usage. These sources of value are competitive and compress over time.

In internally settled environments, economic value becomes more closely associated with balances rather than transactions. Persistent custody, balance sheet efficiency, and yield generation take on greater importance. Transaction-based revenue declines, while new forms of balance-driven value emerge. Market participants may therefore need to reconsider their strategies, moving away from volume-based models toward those that emphasize balance management, yield optimization, and structural efficiency. The opportunity set may expand, but it shifts location within the system.

Boundary Conditions for structural pricing compression

For internal settlement to materially compress FX pricing, several conditions are likely to be relevant:

- Settlement is internal, with finality achieved within a shared custody context.

- Custody persists, allowing balances to accumulate rather than churn.

- Balance sheet economics are durable, providing value independent of transaction volume.

- Execution remains neutral and deterministic, preserving price-based competition.

- Regulatory obligations attach to custody and settlement, rather than to price discovery.

- Liquidity is anchored in operational demand, rather than transient incentives.

Where these conditions are met, pricing outcomes are determined more by system structure than by policy.

Implications for global payments and liquidity formation

The relocation of settlement inside the trading system has implications beyond institutional FX execution. Global payments have historically been shaped by fragmented settlement and the challenge of matching offsetting currency demand across bilateral relationships. Intermediation has evolved to bridge these mismatches and manage the associated balance sheet complexity.

In an internally settled environment, these constraints may begin to ease. Liquidity can be coordinated across a broader network of currency relationships. Matching becomes more system-wide, and less dependent on bilateral alignment.

In conventional systems, balances must move to achieve settlement. In internally settled systems, obligations can be resolved within a shared state. Movement becomes less central, reducing the structural reliance on multiple layers of intermediation in global payment flows. As a result, the role of intermediation may evolve. Pricing improvements arise not only from competition, but from changes in the underlying structure that previously required intermediation.

A historical analogy: The VoIP precedent

A useful parallel can be drawn from the transition from traditional telephony to Voice over IP (VoIP). Legacy telecommunications priced voice according to distance, infrastructure, and interconnection. Costs reflected network structure, not the service itself. VoIP altered this by internalizing communication within a data network. Once voice became data, the marginal cost of transmission declined significantly, and pricing adjusted accordingly. Foreign exchange exhibits a similar dependency. Pricing remains elevated not necessarily because price discovery is inefficient, but because settlement occurs across fragmented external systems. When settlement is internalized, this constraint is reduced. As with VoIP, changes in structure can lead to relatively rapid adjustments in pricing dynamics.

Structural asymmetry and irreversibility

The dynamics described are not fully symmetrical. Systems that internalize settlement and derive value from balances may be able to reduce or eliminate execution costs without compromising sustainability. Systems that remain dependent on external settlement continue to recover costs through pricing. This creates a structural asymmetry that is difficult to offset through incremental improvement alone. Where participants gain access to consistently lower-cost execution within internally settled environments, there is limited economic incentive to return to higher-cost alternatives. Balances tend to persist where conversion is efficient and finality is reliable. Liquidity often follows that persistence. In this context, competition may lead less to convergence between models and more to a gradual reallocation of activity.

The forced binary

Foreign exchange pricing does not appear to converge toward marginal cost through incremental improvement alone. It converges when the economics that fund the system move below the point of execution. As long as settlement remains external, pricing continues to reflect the need to recover associated frictions. When settlement becomes internal and custody persists, those constraints begin to shift.

Execution becomes less central as a source of revenue. Pricing increasingly reflects competitive dynamics rather than cost recovery. Balance-driven economics take on a more prominent role. In practice, the future of FX pricing is likely to be shaped less by incremental adjustments within the current framework, and more by the adoption of structures that redefine where economic value is created and captured. The resulting landscape is less defined by convergence, and more by the divergence of distinct economic models. FX pricing does not compress through competition alone – it compresses when settlement becomes internal to the market itself.