Electronification allows banks to support the growing client demand for more FX swaps trading across multiple currencies and tenors.

Pricing in FX swaps is highly complex due to banks having to provide prices along the forward curve – not just short dates or standard tenors but approximately 250 odd dates as well. Managing this requires sophisticated pricing engines that capture highly fragmented data from many different sources explains Marco Kuper, chief product officer at DIGITEC.

“The market continues to grow in volume while evolving to a more electronic structure,” he explains. “Electronification means clients have improved access to trade FX swaps and banks are able to price the growing volume of RFQs having implemented workflow automation. But the missing piece is the interdealer market, where managing risk is manual because it is still mainly a voice market.”

Automating the capture of market data, analysis, price distribution, trading, confirmation and settlement not only delivers significant efficiencies; it also provides an improved client service.

“Electronification means clients have improved access to trade FX swaps and banks are able to price the growing volume of RFQs having implemented workflow automation.”

Marco Kuper

“Managing FX swaps pricing using Excel spreadsheets has become increasingly ineffective due to client demand, the increased velocity of the market and huge volumes of data,” continues Kuper. “Fragmentation means that many different data sources are needed to price accurately.”

Data a competitive advantage

As new data sources from different markets become available, the more technologically advanced firms are subscribing to this data to give them an information and speed advantage in FX trading.

Electronification’s most important contribution has been its ability to provide price takers with significantly greater execution flexibility and enhanced price transparency. By lowering traditional liquidity barriers, electronification has reduced constraints on balance sheet access, enabling broader and more efficient participation in the market.

That is the view of Jim Norcott, managing director, FX commercial lead, GlobalLINK, State Street Markets, who notes that this improved accessibility has fundamentally transformed the FX swaps market into a scalable, data-driven ecosystem – one where pricing is consistently tighter and execution is materially faster.

“Electronic execution methods enable continuous, real-time pricing visibility and provide clients with more efficient tools for price benchmarking across venues and counterparties,” he says. “This instantaneous view of executable pricing has fundamentally altered the liquidity dynamic, shifting greater control to price takers. With increased transparency and faster access to competitive quotes, clients are better positioned to assess market conditions, compare pricing in real time, and execute with greater confidence.”

“Multi-dealer platforms enable a range of high volume, low-touch execution methods that allow clients to scale trading activity without a corresponding increase in operational overhead.”

Jim Norcott

Automation has delivered meaningful cost and workflow efficiencies across the FX swaps execution lifecycle by significantly reducing the need for manual intervention and minimising the implicit costs associated with voice-based execution. By shifting activity toward automated, rules-based workflows, clients can execute more efficiently while reducing operational friction.

“Multi-dealer platforms enable a range of high volume, low-touch execution methods that allow clients to scale trading activity without a corresponding increase in operational overhead,” adds Norcott. “In addition, straight-through processing (STP) for post-trade affirmation and confirmation improves processing speed, lowers operational risk and materially reduces settlement risk.”

When enhanced electronic execution is combined with automated post trade workflows, end to end processing becomes more consistent and resilient – reducing operational errors, accelerating settlement timelines and providing greater transparency into counterparty and market exposures.

Norcott observes that these integrated capabilities allow risk to be managed proactively and systematically rather than reactively. Clients benefit from improved visibility into their positions and obligations, contributing to a more stable and resilient market structure.

Dealers face operational challenges

Adam Cope, head of e-forwards at Deutsche Bank refers to increased demand for electronic pricing in the FX swaps market but adds that innovation as a means for equivalent electronic hedging hasn’t kept pace.

“This means dealers are still faced with the challenge of how to quote and distribute pricing electronically to clients, without a scalable way to auto-hedge or electronically hedge FX swaps or their underlying risks, in interest rate and cross-currency exposures across all currencies and the curve,” he says.

Nevertheless, Cope acknowledges that risk and volume is increasingly being priced electronically, both on single dealer platforms and multi-dealer venues via the well-established RFQ and streaming via GUI on click-to-trade methods.

“Another challenge lies in the lack of a leading D2D FX swap hedging venue,” he adds. “Without critical mass and broad participation from dealers, we are unlikely to see much progress on this front in the near term.”

“What clients are looking for is a strong distribution channel for both electronic and voice, low and high touch.”

Adam Cope

Clearing in products such as EFRPs has seen growth but its applicability remains limited. The prerequisite for exact tenor matching on IMM dates – as required by definition for futures – means it is only suitable for a small fraction of overall FX swap volume and business, although some clients are migrating rolls onto IMM roll dates, motivated by reduced credit risk via the cleared equivalent.

“What clients are looking for is a strong distribution channel for both electronic and voice, low and high touch,” concludes Cope.

Compared to other parts of the FX market, FX swaps are less transparent, necessitating quotes from multiple liquidity providers to understand where the market is. They are also usually subject to the uncertainty of last look credit checks on electronic trading venues, explains Phil Hermon, head of growth and execution, FX products at CME Group.

“This lack of transparency and particularly the existence of post-trade credit checks has, arguably, hampered the electronification of the FX swaps market,” he says. “However, market innovation combined with the growing impact of capital on longer-dated FX swaps are serving as catalysts for participants – especially banks – to invest in new ways of trading.”

“Market innovation combined with the growing impact of capital on longer-dated FX swaps are serving as catalysts for participants – especially banks – to invest in new ways of trading.”

Phil Hermon

The FX swaps market needs to minimise manual steps, not just post-trade but for the end-to-end workflow, from initiation of pre-trade right through to settlement and post-settlement actions suggests Finteum co-founder and CEO, Brian Nolan.

“This opens up the FX swaps markets to the efficiency we have seen develop in spot FX and equities but also reduces operational risk,” he says. “Several banks have implemented automated processing of trades – we have seen T+0 intraday FX swap trades progress from RFQ to settling the near leg within a few minutes and we are working on reducing that to seconds, without pre-funding.”

SaaS supports rapid updates

Finteum offers SaaS as an option, which means that banks can start trading more quickly than with on-premise or private cloud. “SaaS also means we can keep the system updated more easily and avoid cyber vulnerabilities,” says Nolan. “However, there are other parts of institutions’ technology stack to consider to unlock the FX swap market further. Many have on-premise booking and settlement systems and they are often running old versions.”

“We have seen T+0 intraday FX swap trades progress from RFQ to settling the near leg within a few minutes and we are working on reducing that to seconds, without pre-funding.”

Brian Nolan

DIGITEC works with bank clients of different sizes with different distribution models to identify their evolving needs. One recent example was the launch of D3 Channels, a service designed for trading desks which directly manage client pricing.

“We worked with some of our existing banks to develop the service, which enables traders to establish easily maintainable, rule-based and scenario-based logic that automates pricing decisions based on tier and volume band,” says Darryl Hooker, head of sales and partnerships.

The company has also evolved the way it delivers its software applications and solutions by migrating to SaaS, which makes services more accessible in terms of technology and also cost and allows it to scale solutions and support clients around the world, delivering updates and upgrades more quickly and easily.

“SaaS means that the overall cost of having state-of-the-art FX swaps technology has become more accessible.”

Darryl Hooker

“Since we moved to a SaaS model we have seen significant growth from regional bank clients,” says Hooker. “SaaS means that the overall cost of having state-of-the-art FX swaps technology has become more accessible. Well-designed tools have in-depth expertise baked in and efficient monitoring is available out-of-the-box, allowing smaller trading desks to participate in the FX swaps and NDF market and still be competitive in terms of pricing their clients.”

It also implies a lower overhead for IT departments in smaller banks compared to a legacy on-premise installation, with no need to learn about specialised connectivity requirements.

According to Norcott, electronification has been a key enabler of algorithmic FX swaps trading by transforming what was historically a fragmented, voice-driven market into one supported by real time data, standardised workflows and systematic execution.

Electronic platforms now provide streaming prices alongside consistent request for quote (RFQ) protocols and application program interface (API) connectivity, allowing clients to integrate FX swaps trading directly into automated execution frameworks with minimal human intervention.

“As algorithmic execution adoption increases, price takers benefit from greater consistency, speed and discipline in how trades are executed,” says Norcott. “Algorithms can respond dynamically to market conditions, optimise execution across tenor structures and reduce information leakage relative to manual workflows.”

AI augments human input

He refers to the use of AI in the FX swaps process to help augment human decision making within existing workflows, explaining that it creates a continuous feedback loop where every trade assists in improving future decision making.

“The ability to use decision augmentation tools embedded into workflows brings FX swap automation to an entirely new level. Now clients can navigate their swap liquidity needs more intelligently without the need for any disruption to their standard execution process.”

Meanwhile, advances in technology and the adoption of new delivery models such as SaaS and cloud-based infrastructure have significantly lowered the barriers of entry into the FX swaps market, particularly for smaller banks and institutional participants.

Collectively, these technology-driven delivery models are democratising access to the FX swaps market through broadening participation, improving liquidity distribution and fostering a more competitive and resilient ecosystem where institutions of all sizes can engage more cost effectively and efficiently.

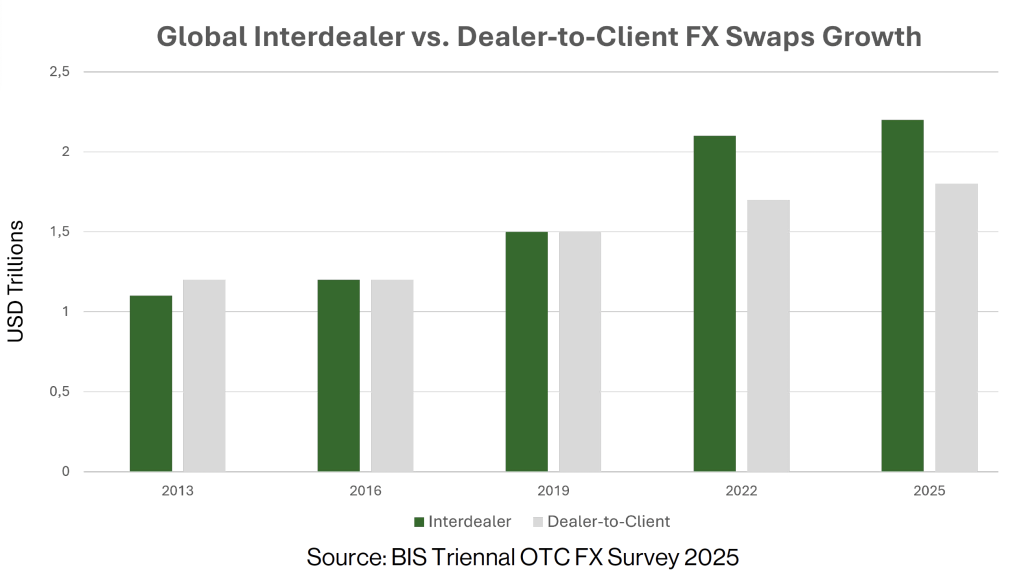

In its whitepaper ‘The Profitability Squeeze Driving FX Swaps Modernization’, 360T notes that ‘the interdealer market has failed to modernise in proportion to its own expansion’.

One of the reasons why the interdealer FX swap market has lagged in electronification is the need for banks to price one another transparently and continuously – something fundamentally different from dealer-to-client workflows, explains Robin Nicholas, head of FX swap product at 360T.

“Streaming firm prices can reveal trading intent and balance sheet usage, making participants understandably cautious – particularly in episodic, balance sheet-intensive markets,” he says. “There have also been concerns around price recycling and spread compression without guaranteed execution.”

However, Nicholas notes that these challenges are increasingly being addressed through more nuanced electronic models, such as matching at mid in dark pools, which allow banks to access liquidity and achieve price improvement without fully exposing their positions.

It is also worth noting that banks, despite competing across the broader FX landscape, face challenges in building an interdealer platform that meets all participants’ needs.

Reducing the administrative burden

The whitepaper also referred to the capacity for electronification to reduce the administrative burden of FX swaps activity.

“Manual FX swaps trading carries a significant administrative burden across the full trade lifecycle,” says Nicholas. “Pre-trade, interdealer FX swaps rely on manual, fragmented bilateral credit checks. Participants must coordinate with counterparties over voice or chat to source prices, interpret non-standardised quotes and structure trades using spreadsheets, often while maintaining informal records for audit purposes.”

Electronification addresses these challenges by embedding credit controls directly into the execution workflow.

“Post-trade, the burden intensifies with the generation and matching of confirmations, the resolution of discrepancies with counterparties, the management of settlement instructions and ongoing reconciliation between internal books and external records,” adds Nicholas.

Looking ahead, he says the adoption of clearing solutions could further streamline post-trade workflows by reducing bilateral exposures altogether, significantly lowering the administrative burden associated with credit, confirmation and settlement management.

Nolan observes that participants may have limited budget to pursue electronification and many regulatory projects to deliver on. “Credit is often cited as an issue but this has been solved – institutions just need to adopt the solutions,” he adds.

“Manual FX swaps trading carries a significant administrative burden across the full trade lifecycle.”

Robin Nicholas

Kuper thinks the interdealer market needs to migrate to electronic FX swaps venues. “As these venues attract more liquidity and interbank-quality data becomes more widely available, we expect this to drive increased liquidity across the whole FX swaps market, which in turn will lead to greater participation, and improved client pricing and risk management,” he says.

Like the rest of the market, workflow automation is vital for interdealer venues to grow. “Banks need specific workflows – such as supporting nuanced order placement – so that when a trader’s curve moves their prices update automatically. Workflow automation means the dealer can stream their interest downstream to clients and to the venues, while dynamically managing the amounts and prices shown on each channel” says Kuper.

As for the factors that may hinder full electronification of FX swaps, Norcott acknowledges that they remain constrained by balance sheet and bilateral credit.

“In particular, rising capital and risk-weighted asset (RWA) costs mean that liquidity provision in swaps is increasingly governed by balance sheet optimisation rather than pure market opportunity,” he says. “While platforms have made progress through pre-trade credit checks, dynamic limit management and smarter workflow controls, these measures can only partially offset the underlying economics when credit becomes scarce.”

More to be done

Market dynamics also play a role. During periods of volatility or balance sheet stress such as quarter ends or regulatory reporting windows, liquidity providers may pull back risk capacity or revert to more discretionary, voice based execution.

“Until balance sheet efficiency, credit intermediation and capital transparency evolve further, these structural and market frictions will continue to temper how far and how fast the FX swaps market can move toward full electronification,” adds Norcott.

Progress will also depend on closer collaboration between trading platforms, liquidity providers, clearing infrastructure and regulatory bodies to align incentives and encourage broader adoption of these solutions.