Tim please could you share a brief overview of your career journey in FX and electronic trading to date?

I have been fortunate to have a 2-decade career in FX across sales, e-FX product and Trading. This has included the build out (and re-build out) of the e-FX capability covering pricing, distribution and risk management. I have been fortunate to be at the forefront of doing this from within the African continent, so I have been able to experience what it takes to implement a global best practise model but tailored for the nuances of emerging markets.

Doing it within the bank has also given me an appreciation of the various clients sets that a regional specialist services from offshore investors and hedge funds to the global multinational, local corporate as well as retail clients across person and high net worth. I have also had the privilege of doing this across various African countries giving me a true appreciation of the uniqueness of the continent which has currencies like ZAR all the way to NGN which each have their own dynamics.

What is your current role at RMB, and what are the key responsibilities of you and your team?

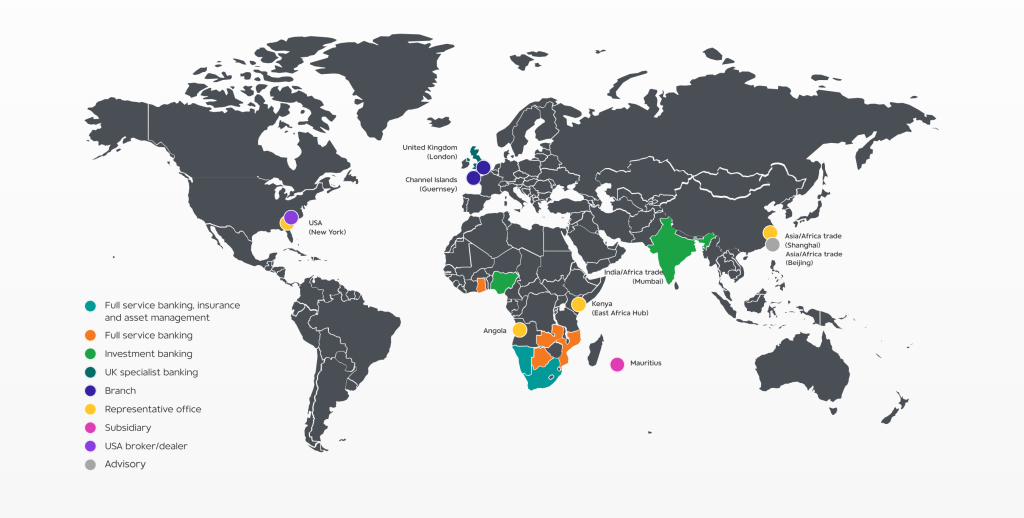

I am the Head of Global FX and Electronic Execution for RMB (which is part of the FirstRand Group) which focuses on the liquidity management and trading of all major liquid currencies across spot, forwards and derivatives. In addition, I am responsible for the core FX platform including the pricing engine and distribution capabilities for all entities and client segments.

As a group we run a centre of excellence model and as such for our outside of South Africa business, we support our local in-country teams to market make their local currencies into the platform to enable broad distribution.

In addition to FX, I have a broader Electronic Execution mandate which is focusing on transforming more of the bank’s asset classes along the digitization and electronic journey such as Fixed Income and Commodity trading.

Transforming a trading business with new digital workflows, automated pricing, market making, and risk management is challenging. How critical is collaboration across your Trading, Product Management, Quants, and Client Services’ teams in order to achieve that objective?

We have been a later mover as RMB and as such the buy in to transform is there. The digital transformation though is as much a people exercise as any other. Working with strong, successful people requires huge amount of trust between people where questioning requirements and suggesting alternatives needs to be embraced. Taking a design lens to any transformation is critical so that legacy processes and ways of work can be questioned so that new capabilities are not implemented on old processes. Each part of teams helps think of solutions in a continuum which makes new solutions scale better.

What are RMB’s core electronic FX offerings and how does your unique liquidity proposition differentiate the bank from other supraregional players?

We have invested heavily in our capability over the past few years which has included a complete overhaul of our FX stack across our trading and sales business. As a result of this, we have a world class pricing and distribution capability where we can meet clients where they need, over the venue they wish in the location they desire.

Through our investment into key technology partners we believe we have a capability comparable with many tier 1s. We have not only implemented the capabilities but equally transformed our teams with an “e-FX First” approach meaning that everything we do is run through the e-FX stack which includes many of the non-liquid activity which may be concluded off platform but ultimately is booked through the system to ensure we get the benefits of the control and data that the e-FX stack provides.

Through this work we apply a strong focus on quantitative research which has allowed us to design our offering completely around the importance of us as a primary market maker to our franchise and the role we play in the market. This means that our pricing models offer a truly unique opportunity for people to access onshore local liquidity. We believe this makes us unique on the continent, but we also appreciate that this will evolve and as such I am very proud of the architecture we have built that allows us to scale into new opportunities.

A key focus for us this past year has been evolving our FX SWAP as well as NDF solutions. While these markets are themselves evolving, we are proud that we electronically price and distribute our products widely across all major platforms and are actively looking at ways to continue expand our solutions. The demand for these products continues to grow (from our offshore investor client base) and the fact that we have made this capability available electronically is a big differentiator for us.

What are some of the key growth drivers for African e-FX and how are they helping to transform the continent’s financial landscape from fragmented markets to a more integrated e-FX ecosystem?

The biggest focus for decades has been payments into and out of the continent. While this largely is spoken of in context of remittances and retail flows, it is a systemic issue that has been experienced by all segments. While e-FX has made access to price discovery easier, the settlement and payment processes do remain a challenge.

While modern technologies like Blockchain and the rise of stablecoins appears to be a very promising development this has yet to meaningfully transform the economies. The major financial institutions within the continent (including RMB) have a significant part to play in enabling Africa’s growth. Particularly as it pertains to the e-FX capability, we are focused on the entire value chain of the FX flows from pricing and liquidity through to settlement and ultimate beneficiary acceptance.

As RMB our investment in the e-FX stack has allowed us to focus on ensuring that our distribution can quickly respond to new requests such as the ability to source pricing for information or payment providers looking for ways to book into Africa.

Secondly we have ensured that our solutions are entirely API native meaning that we can meet new payment providers and solutions at their place of transaction and finally leveraging the e-FX stack normalizes the straight-through-processing into various downstream settlement and reporting systems.

By making it easier to access liquidity and pricing in African currencies while ensuring we can effectively link into settlement systems and be clear on reporting has started to see much more interest in how to solve these challenges. We are actively working with several fintechs as well as our own internal areas in how better to promote these into the core offerings.

On an adjacent approach we have focused in promoting ourselves as regional specialists with many of the global banks as well as major investors offshore. This work is important as allowing them to see the ability to transact and source liquidity through scaled channels (enabled through e-FX) makes doing business in Africa seem more feasible.

This has been a significant source of growth for RMB and we already see many of the major trading venues reporting us as a significant market maker in USDZAR. We are now actively expanding this into other African Deliverable and Non-Deliverables pairs. By being active in the market and promoting our regional expertise we see a natural second order effect of investors seeking trading opportunities in local bonds and where we as an organization are well placed to respond.

With the global NDF market growing rapidly, what steps has RMB taken to advance electronic non-deliverable forwards (NDFs) trading in your region of the world?

This is one of the areas I am very excited about and encouraging for us we have extended our e-FX first approach to NDFs. At RMB we have a very forward-thinking team market making African NDFs and the need to meet more clients on their chosen platform is key to them. We have enabled our team through great technology for both price construction and distribution and we currently market make over 8 African NDFs on our platform and distribute these onto a few of the major trading venues.

While larger transactions still currently go through our sales desk, but we have enabled them to use our Single Dealer Platform for all aspects of pricing and booking of deals. This in turn then ensures that post-trade workflows run seamlessly and timeously. Investor clients appreciate the efficiency in our execution and opens more conversations for platform distribution. By facilitating through the e-FX stack also allows us to gather valuable data around our NDFs – which is a source of our continuous evolution.

The use of FX algorithmic execution and associated services is also growing. How much demand are you seeing for it from clients and what work has RMB been doing to develop your own quantitative FX capabilities?

I had hoped that this would have grown more within the local client base than it currently has. To this extent the largest number of enquires we receive are from offshore clients who are used to these solutions offered by their global banks. The reality for a local institution is the cost of implementation is extremely high, not purely because of the cost to set up such a solution (including if done on a white-label basis), but more so how to navigate this in terms of internal prioritization.

Given that many banks run lean technology teams who also (generally) have the mandate of supporting the broader FX transactional needs, it is hard to re-direct this capacity for the algorithmic build out.

At RMB we have made the call to be e-FX first and one of the more interesting developments has seen our e-FX trader being the key source of market colour and insight into our sales teams and in turn to clients.

The views produced by our e-FX trading team has sparked a keen interest by salespeople and clients alike in how we view liquidity, our measurement of client flows and general techniques in achieving optimal execution.

Many of the local client understanding of market dynamics is anchored in the primary market activity (exclusively) and the insights provided by our e-FX trading team have been a huge source of understanding for many.

These e-FX quantitative techniques have been incorporated into research ideas and client specific reports which has opened many new conversations. A general curiosity has emerged on liquidity management, mark-outs and overall internalization rates and how to optimise these. These insights expose many more people to how the market has evolved and our approaches to our own executions and internalization.

Lastly, I have been delighted in our technology partners who have enabled us through native algo containers and frameworks that has sparked internal curiosity on execution algos.

This capability has been a significant source of inspiration for our quants and allowed us to build out our own pricing and execution approaches on the platform.

We are actively working on this and do expect that more clients will embrace these solutions in the near future.