The latest BIS FX survey confirmed what many participants and fintech’s across the market already knew – FX options are becoming one of the fastest-growing segments of global foreign exchange trading. As a reminder FX Options Average Daily Volume (ADV) doubled according to the BIS report from 2022 to 2025 at $634 billion.

While spot and swaps FX remain enormous, the strategic energy increasingly sits elsewhere — in volatility, optionality and more sophisticated hedging and trading workflows. As macro volatility, rate divergence and geopolitical uncertainty continue to drive demand for hedging instruments, the FX options market appears to be entering a new phase of electronification.

That raises a larger strategic question for the industry.

As FX options trading becomes more electronic, does the market consolidate around the large multi-product FX platforms? Or do options remain a specialist workflow where niche providers such as Digital Vega and OptAxe retain defensible positions?

History suggests both outcomes are possible.

In some electronic markets, scale and network effects eventually overwhelmed specialists. In others, complexity preserved fragmentation and allowed niche firms to thrive alongside larger incumbents. FX options now appears to sit directly between those two paths.

Why FX Options is growing

The structural drivers behind FX options growth are relatively clear.

First, the post-2020 macro regime has fundamentally changed hedging behaviour. Higher interest rates, larger FX swings and more persistent geopolitical uncertainty have increased demand for optionality across both institutional and corporate client segments.

Second, volatility itself has increasingly become an investable asset class. Many of the macro hedge funds and banks I meet talk about the increase in systematic volatility strategies and relative-value trading across their firms. Most product client types (banks, asset managers, corporates, etc) have all expanded their activity in FX volatility markets over the past decade.

Third, dealer technology has improved materially. Pricing engines, automation tools and RFQ/RFS infrastructure are now significantly more sophisticated than they were even five years ago. Products that historically required heavy voice interaction can increasingly be traded electronically, particularly in G10 vanilla options. As the technology becomes more mainstream many more Liquidity Providers (LP’s) are happy to start to integrate pricing across multibank FX platforms. At the same time there has been a large reduction in transaction revenue rates on platforms as LPs squeeze them in negotiation with their pricing feeds. Some platforms continue to try and hold firm on higher vanilla option transaction fees but it’s just a matter of time. Platforms are just stalling option transaction revenue reductions to balance the books on their revenue growth projections to investors and ownership.

Finally, buy-side firms themselves are becoming more comfortable with electronic options workflows. Many traders have grown up in increasingly multi asset electronic markets – rates, equities and listed derivatives. Expectations around execution, workflow integration and data transparency have evolved accordingly.

The result is that FX options are beginning to move from a relatively specialist corner of the market toward a more scalable electronic business. It’s easier for fintech’s to access the market as technology builds get cheaper and more Dev efficient with the introduction of AI into the Dev space.

Does that transition ultimately favour the largest platforms (Bloomberg, FX Connect, FXAll, etc) or the more specialised ones (Digital Vega, OptAxe, etc).

The case for consolidation

The argument for consolidation is compelling.

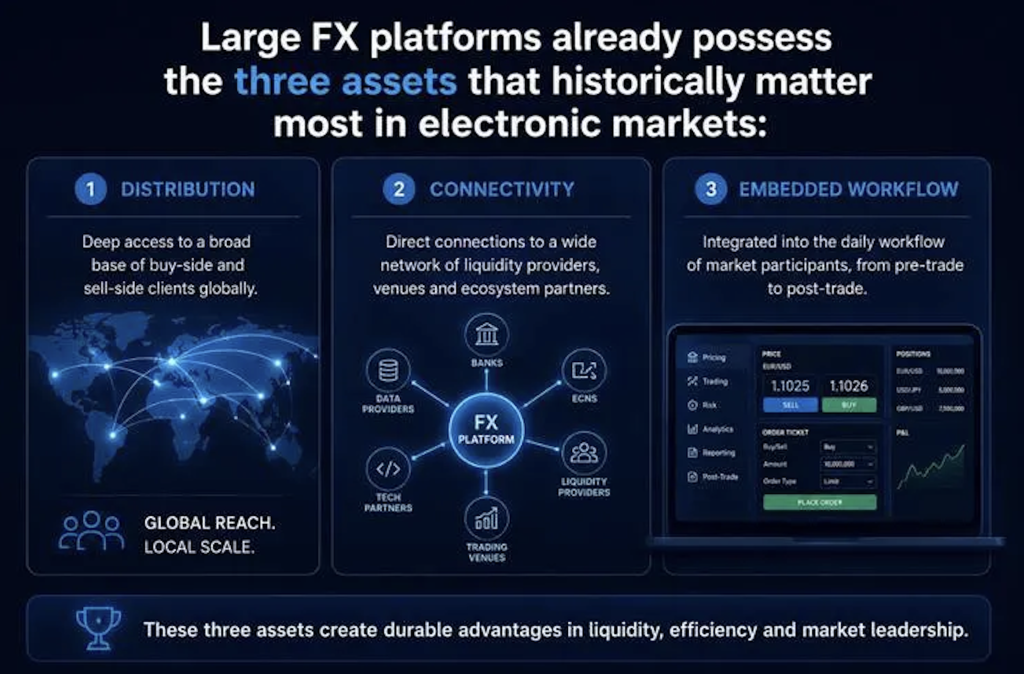

Large FX platforms already possess the three assets that historically matter most in electronic markets: distribution, connectivity and embedded workflow.

Firms such as the large ones mentioned above already maintain deep client relationships across spot, forwards, swaps and some in such as LSEG and Bloomberg in broader fixed income workflows. Extending those relationships into FX options appears strategically logical.

Clients themselves increasingly prefer workflow consolidation. Asset managers and corporates alike are under constant pressure to reduce operational complexity, simplify vendor relationships and integrate execution with compliance, analytics and post-trade systems. For many institutions, “one more specialist platform” carries a real operational cost and regulatory risk. That dynamic has played out repeatedly across electronic markets over the past two decades.

Electronic cash equities provide perhaps the clearest historical parallel. In the early days of ECNs and alternative trading venues, fragmentation flourished. Specialist venues emerged with differentiated functionality and unique liquidity pools. Yet over time, network effects began to dominate. Liquidity attracted liquidity.

Large exchange groups and platform operators consolidated the market through a combination of acquisition, integration and scale advantages. Firms such as Nasdaq, NYSE and Cboe Global Markets expanded aggressively as electronic trading matured.

There are obvious parallels with FX.

The major exchange and infrastructure groups have already spent years acquiring FX businesses and workflows, as I have written about previously:

- CME acquired EBS

- Deutsche Börse acquired 360T

- SGX acquired BidFX

- LSEG acquired Refinitiv

These were not simply revenue acquisitions. They were strategic bets on workflow ownership and capturing data points. If FX options ultimately becomes a highly scalable electronic market, the logic points toward consolidation around the firms already controlling the broader FX ecosystem.

I would argue Vanilla options flow, appears vulnerable to this outcome. As pricing becomes more standardised and execution increasingly automated, the competitive advantage may shift away from specialist workflow design and toward distribution scale and liquidity aggregation.

In that world, the largest platforms become increasingly difficult to displace. However, there are 2 parts to this argument.

Why specialists may still win

Yet the counter-argument is equally strong.

FX options are not spot FX. Spot FX is fundamentally a speed and liquidity business. Options trading is a workflow and risk-transfer business. The priorities of an FX options trader differ materially from those of a spot trader.

Options participants care about volatility surfaces, skew dynamics, structuring flexibility, liquidity discovery and RFQ sophistication. Execution quality is often less about raw speed and more about information, negotiation and workflow precision. That complexity may protect specialist firms.

This is where the comparison with electronic rates and credit markets becomes more relevant than equities. Despite years of electronification, fixed income and derivatives markets did not fully converge into a single winner-takes-all platform structure. Instead, specialist workflow providers retained meaningful positions alongside larger incumbents.

Firms such as Tradeweb and MarketAxess succeeded not simply because they aggregated liquidity, but because they understood the intricacies of dealer-client workflow in complex OTC markets. Electronic execution did not eliminate fragmentation because the underlying products themselves resisted commoditisation.

FX options shares many of those characteristics.

Large portions of the market remain episodic and relationship-driven. Liquidity is often nuanced rather than continuous. Pricing models, dealer axes and structuring expertise still matter enormously.

That creates room for specialist firms such as Digital Vega and newer entrants such as OptAxe to build defensible positions despite the presence of far larger competitors. In fact, I would argue specialists may possess structural advantages precisely because they focus narrowly on options workflows. We built and successfully sold BidFX on the back of a narrow focus on complex hedge fund workflow knowing this was an area more generic platforms couldn’t compete with.

Specialists can iterate faster. They can tailor functionality more aggressively around the needs of volatility traders. They can optimise RFQ logic, dealer interaction and analytics in ways that broader platforms may struggle to prioritise internally. In electronic OTC markets, depth of workflow often matters more than breadth of coverage.

That has repeatedly allowed niche firms to survive longer than many observers initially expected.

The most likely outcome: Bifurcation

The most probable outcome for FX options is neither complete consolidation nor permanent fragmentation. Instead, the market may bifurcate.

Highly standardised G10 vanilla flow is likely to become increasingly consolidated and electronic over time. That segment naturally favours large platforms with scale, distribution and existing client connectivity.

More sophisticated and complex workflows, however, may remain specialist for far longer. Structured products, multi-leg strategies, EM options and nuanced volatility trading workflows are less easily commoditised. Those areas may continue to reward firms with deep domain expertise and highly specialised execution tools. This hybrid structure already exists across multiple electronic asset classes.

The more interesting question may therefore not be whether specialists survive, but whether they eventually remain independent.

History suggests many successful workflow innovators ultimately become acquisition targets rather than long-term standalone challengers. That pattern has repeated itself across FX, equities and fixed income markets for two decades. Smaller firms innovate around workflow friction; larger infrastructure providers later industrialise and distribute those innovations at scale. The recent history of electronic trading is full of such examples.

FX options may simply be the next chapter in the same story. As the market grows, workflow ownership — not just liquidity ownership — is likely to become one of the most strategically valuable assets in global electronic trading.

John McGrath’s Substack page can be found at: https://substack.com/@johnmcgrath616049