Payment versus payment (PvP) is the ideal solution for eradicating settlement risk but where this isn’t (yet) possible the market needs to consider all options and technologies. We spoke to Andrew Harvey, Managing Director Europe of the GFMAs Global FX Division.

The Global Financial Markets Associations (GFMAs) Global Foreign Exchange Division (GFXD) was formed in co-operation with the Association for Financial Markets in Europe (AFME), the Securities Industry and Financial Markets Association (SIFMA) and the Asia Securities Industry and Financial Markets Association (ASIFMA). Its members comprise 24 global foreign exchange (FX) market participants , collectively representing a significant portion of the FX inter-dealer market. It is these members that are most exposed to settlement risk, particularly that which falls outside of PvP via CLSSettlement. Consequently, over a number of years, the GFXD has been examining possible solutions and remedies for settlement risk and contributing to high-level discussions with central banks, policy makers and other market and industry representatives.

In 2018, The GFXD’s Recommendations for Settlement Netting1, explained how settlement netting can reduce settlement risk for those trades that settle outside of CLSSettlement. “In our view,” Andrew Harvey explains, “the counterparties to trades, should try to use settlement netting wherever they can. We are very much in agreement with the FX Global Code’s principle 50 which specifically states that market participants should measure and monitor their settlement risk, seek to mitigate that risk where possible, and talks about FX settlement netting and encourages that.”

Summary of GFXD’s recommendations for Settlement Netting

How this is best done is the crux of the matter. Harvey reiterates the points made in the paper that counterparties need to agree at the outset, at onboarding, how trades will be netted and adhere to the agreed process on a consistent basis. This however is not perfect for two reasons in particular. Firstly, that a settlement of the netted amount still needs to be made and although the amount may be less the settlement risk is still present. Secondly, Harvey makes the point that in-house operational systems are set to be as efficient as possible to settle on a net or gross basis. Switching between these, perhaps on an ad hoc basis, can introduce a measure operational risk.

New technology and interoperability

From a strategic point of view the GFXD would like to see as much flow in the market settled through PvP as possible simply because it is the tightest possible response to settlement risk. It’s paper on expanding PvP2 sets out its position. However, recognising that this is not always possible, the GFXD awaits further analysis from the BIS, CLS and others to learn more about the character and composition of the residual settlement risk existing in the market.

Summary of GFXD’s recommendations for the reduction of systemic Settlement Risk through the promotion

of settling wholesale FX transactions on a Payment versus Payment (PvP) basis.

New technologies and market behaviours may point the ways ahead. For example, extending the time windows of central bank real-time gross settlement systems or new technologies such as wholesale central bank digital currencies– all of these have merit the GFXD argues. However, its concern is that there needs to be interoperability3. As a global market with many participants continually interacting with each other it is essential that their systems and procedures match. Unless this is enabled, Andrew Harvey says that new technologies may not be best suited to the market though it is an evolving picture.

He asks, “Is it a case of doing things better today, or of using new technology to do things better than today, or is it a mix of the two? I think, when you start looking at FX, being by definition cross-border, you need the two jurisdictions to engage, and then you start looking at the efficiencies of scale and funding and liquidity provision. It needs to be more than two central banks however. I think that’s where the CPMI (The Bank for International Settlements’ Committee on Payments and Market Infrastructure) work on enhancing cross-border payments is well received, and is exactly the right place to start thinking through some of these scenarios. We’re always happy to engage with them on this and to provide feedback where helpful.”

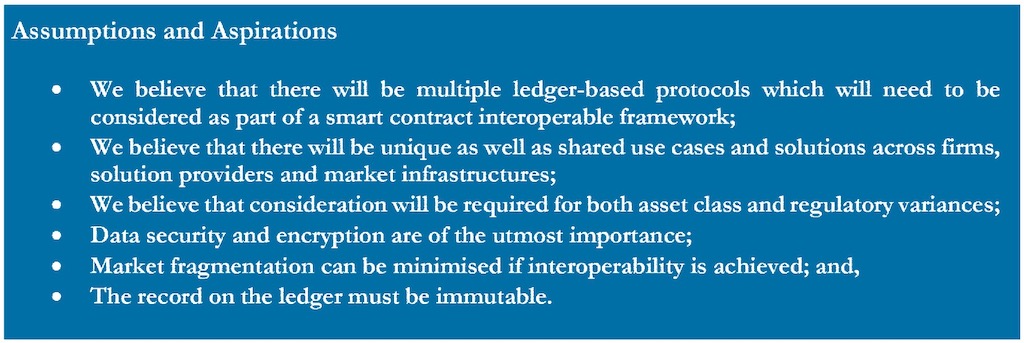

The GFXD has identified several assumptions and aspirations which they believe are fundamental in the

consideration of new technologies/services within the area of global FX and cross border payments

Andrew Harvey concludes by reiterating the goal of further de-risking the global FX system through increased use of PvP. “I think that is where the industry is ultimately looking to move to. I think the timeframes for achieving that will largely depend on the opportunities that are out there, either through existing services or new technologies that are being developed.”

- GFXD recommendations for FX Settlement Netting https://www.gfma.org/policies-resources/gfma-fx-division-recommendations-for-fx-settlement-netting/

- First Steps Towards 24/7 FX Settlement Capabilities – Expanding Payment versus Payment (PvP) opportunities https://www.gfma.org/policies-resources/first-steps-towards-24-7-fx-settlement-capabilities-expanding-payment-versus-payment-pvp-opportunities/

- GFXD recommendations for the promotion of interoperability between new technologies and service providers https://www.gfma.org/policies-resources/gfxd-recommendations-for-the-promotion-of-interoperability-between-new-technologies-and-service-providers/